Banking is evolving towards a commercially and technologically more open model, Open Banking. To build customer loyalty in such a highly collaborative and competitive environment, banks need to move away from the "salesman" approach. They must learn to create new customer experiences. Managing customer consent and the transferability of that consent in an open ecosystem will be a key element in preserving the trust that customers place in their bank today.

|

Key ideas to bear in mind:

|

Summary:

What is Open Banking?

In an increasingly digital and competitive world, Open Banking is a model of the bank of the future.

It is an open bank that prioritises the sustainability of its relationship with its customers over the sale of in-house products. To retain customers, banks enrich their offer by collaborating with value-added partners, or even competitors. They position themselves as a platform at the centre of a collaborative ecosystem.

Initially, the external services offered may be complementary banking services, such as mobile payment services offered by innovative start-ups.

Eventually, the bank may open up to non-banking services such as property management services or even the sale of consumer goods. It may also take the step of offering competing banking services, thus becoming a true marketplace.

Why is Open Banking the future of banking?

For large banks who are used to selling in-house products to captive customers, Open Banking is a revolution.

For Ronan Le Moal (with whom we did a webinar, in French, in June 2021), who has spent 25 years in the banking industry, including the general management of Crédit Mutuel Arkéa, this revolution is inevitable. According to him, Open Banking is driven by four basic trends:

-

The 2008 crisis marked the end of banks' comfortable margins. They now have to reinvent their business models.

-

The crisis has also brought out the mistrust of consumers. Thanks to the internet, customers have regained power.

-

New competitors, the Fintechs, are nibbling away at the banking market from all sides by responding to new expectations.

-

Finally, regulation has opened a huge gap in the banks' hold on their customers.

In Europe, regulation plays a very important role in opening up banks to competition. The second Payment Services Directive (PSD2) obliges banks to open up access to their customers' banking data to approved external service providers, subject to the customer's consent and the security of this data.

The law stipulates that this access must be offered via APIs (Application Programming Interfaces) that comply with internet standards. With these standards, companies can make their applications interact without changing their respective IT systems. For example, merchants use APIs to display their products on an online marketplace.

Open Banking is therefore a commercial opening of the banking market supported by the technological evolution towards open standards.

|

Whitepaper: Didomi for banks Why is consent & preference management so crucial in the banking sector? PSD2. GDPR. The 8 letters that changed the financial services sector. Discover the true value of compliance and how to turn consent into a critical competitive differentiator in this whitepaper.

|

.png?width=3312&name=WHITEPAPER%20-%20Banking%20-%20Resources%20Page%20(Rectangle).png)

Why is customer data a key issue in Open Banking?

Banks have always had access to their customers' most personal and confidential data: their income, their expenses, their savings behaviour... But where have they put it?

As Ronan Le Moal points out, banks have so far used this data mainly for the narrow purpose of selling products. They have analysed risk in order to sell loans and savings capacity in order to place savings books and life insurance.

In a world where Google, Amazon and other GAFAs are using people's data to not only understand, but more importantly predict their every move, this narrow focus is no longer possible.

Banks must therefore urgently develop their use of customer data and the sharing of this data with a selected ecosystem of partners. This will enable them to build customer loyalty through experiences that are enhanced by partner services and personalised with their data.

As CEO of Gold Circle, Julien Mas is part of the emerging ecosystem of open banks. Gold Circle is an approved information service provider under the PSD2 regulation.

The young company offers consumers the opportunity to authorise access to their banking data so that brands, with their approval, can analyse their purchasing behaviour and offer them personalised services.

In return for access to their data, the consumer receives a reward or refund, for example from 3% to 8% of the value of their purchases. This is known as cashback.

This service gives the consumer back control over their data and, therefore, over their consumption. It offers a fairly unlimited number of opportunities for intelligent consumption services such as directing consumption towards responsible companies or measuring one's carbon footprint.

What is the main asset of banks in their transition to Open Banking?

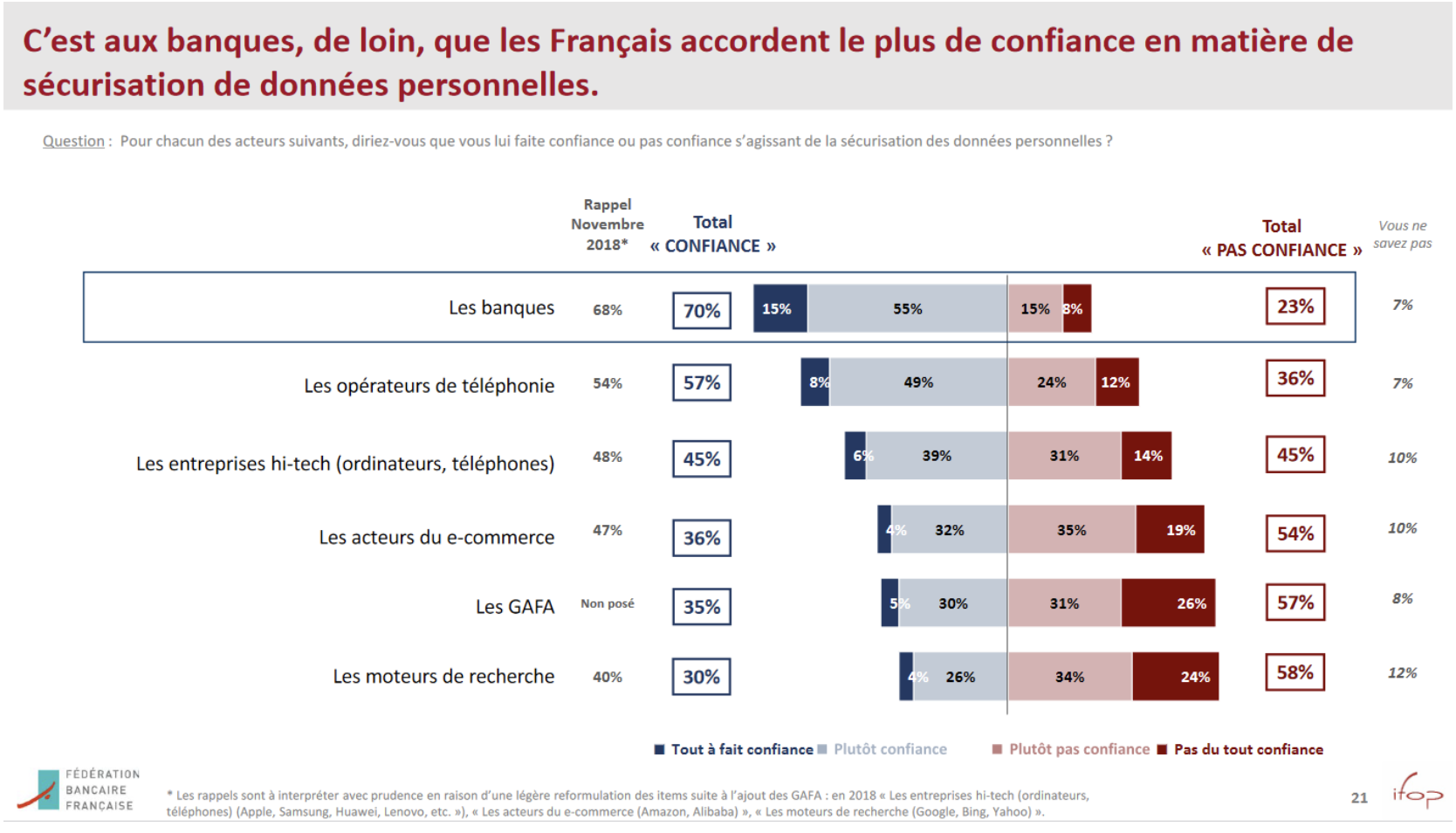

Transactional data is a major asset of banks. They are now obliged to share it. However, as Yannig Roth points out, banks have a second major asset in the transition to Open Banking: consumer confidence.

Indeed, although the French are sometimes mistrustful of the banking sector in general, 88% of them trust their bank. And above all, most of them (70%) trust banks for the security of their personal data, far ahead of telephone operators (57%) and GAFAs, which are trusted by only 35%.

Source: The French, their bank, their expectations

How to capitalise on this trust in an open banking world? How do we convince banking customers to share their data through the banking platform? And how to ensure that this consent is respected in the partner ecosystem?

Many laws currently regulate the use of customer data. The most important of these is the General Data Protection Regulation (GDPR) which limits the use of personal data in the European Union.

The GDPR requires, among other things, that procedures be put in place to allow individuals to exercise their control rights over the use of their data. It puts an end to certain uncontrolled practices of placing cookies and trackers without the users' knowledge.

Customer consent has become an imperative. It has led to the emergence of new actors specialised in consent management systems, Consent Management Platforms (CMPs) such as Didomi.

Didomi’s technology enables banks to manage user consent and preferences relating to the use of personal data at every stage of the customer journey, maintaining an audit trail of customer consent, as well as knowing how to reach their customers, how often, and with the level of advice they expect.

For Didomi, as for banks engaged in the transition to open banking, consent management is not just a legal imperative. It is a way to create value for the user by using data in accordance with their wishes and thereby maintaining their trust.

Where are banks currently in their transformation?

Banks are moving towards Open Banking in a rather forced and coerced way. They are still often at the experimental stage, for example through cooperation with Fintechs in the field of payments or account aggregation.

Opening up the bank involves trial and failure. It requires heavy investments whose return, as Ronan Le Moal points out, is not immediate.

However, investments in the enhancement of customer data and the management of customer consent will be two indispensable elements in the future of the banking industry.